PP047

Why Private Credit Is Creating Unique Opportunities for Passive Real Estate Investors

A few months ago, as I scrolled through loan term sheets for an apartment deal we were pursuing, I couldn't help but shake my head at how dramatically things have changed.

Back in 2021, getting 80% LTV on a quality apartment building was not out of the question. Today? We're lucky to see 65% - and that's on the good days.

But this isn't just happening to us. Since the Fed started raising rates in 2022, traditional lenders everywhere have pulled back hard, creating a massive gap in the real estate lending market.

Loan Supply/Demand Imbalance

While the supply of traditional lending has shrunk, that hasn’t changed investor appetite for rental housing deals.

Why? A few key reasons:

- We're massively underbuilt on housing

- The “own vs. rent” gap is at historic highs

- Other affordability issues are pushing people toward renting

These factors aren't going away anytime soon.

And while fewer deals are trading now than in 2021, the dramatic pullback by lenders has produced an imbalance between the supply and demand for debt on the deals that are happening.

This mismatch – restricted lending supply but strong loan demand – creates an interesting opportunity in a space known as private credit.

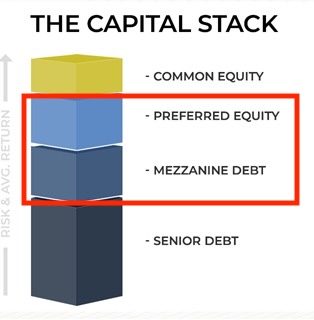

What is Private Credit?

Think of private credit as the middle child of the capital stack family.

It's not as conservative as senior debt (bank loans), but it's also not as risky as common equity (where most syndication investors typically invest).

It usually takes the form of mezzanine debt or preferred equity – both of which sit in that middle portion of the capital stack.

What makes this space particularly interesting is its flexibility. Since it's business-to-business lending without heavy regulation, deals can be structured in ways that benefit both sides.

For borrowers, this means creative deal structures and faster closing times. And for the lenders (and their passive investors), this means better protections for their capital.

The Returns Story

Private credit is generating some compelling returns right now.

I've been analyzing a number of private credit funds lately, and it’s common to see projected cash flow yields in the double-digits – the kind of returns you'd typically associate with junk bonds, but with real estate as collateral and stronger investor capital protection.

Even better? These funds can typically offer:

- Monthly cash flow distributions

- Potential profit participation on the upside

- Shorter illiquidity periods (typically 2-3 years)

- Various fee streams that boost investor returns

Built-in Protection

One thing I love about private credit is how the deals can be structured to protect investor capital:

- Getting paid before common equity

- Real estate as collateral with actual liens on property

- Takeover provisions if performance benchmarks aren't met

- Enhanced reporting requirements keep deal operators accountable

Historically, this kind of investing was reserved for massive institutions writing huge checks. But that's changing. The void left by traditional lenders has created space for more nimble funds that can work with individual investors.

Is Private Credit Right For Your Portfolio?

If you're looking to triple your money in 2 years, private credit probably isn't your play.

But if you're focused on strong cash flow with enhanced downside protection, it could be really interesting.

It's especially well-suited for investors who:

- Want frequent cash flow

- Understand basic real estate fundamentals

- Want higher yields than traditional fixed income

- Are comfortable with some illiquidity (usually 2+ years)

- Are looking to diversify beyond pure equity positions

The Bottom Line

This opportunity exists because of a unique moment in the market. Traditional lenders have pulled back, but the fundamental demand for real estate capital remains strong.

It's not often you get the chance to step into a space traditionally dominated by institutions. And it's even rarer to find an investment that combines strong cash flow with enhanced downside protection.

But this window won't stay open forever. As market conditions normalize, traditional lenders will return and the opportunity will shrink.

For investors seeking strong cash flow with enhanced downside protection, there may never be a better time to explore private credit than right now.

Found this valuable? Join hundreds of sophisticated investors and receive these insights direct to your inbox every week.