PP018

Mastering the Commercial Real Estate Capital Stack

I don’t know about you, but the first thing that comes to mind when I hear the word “stack” is a big plate of Cracker Barrel pancakes.

A big dollop of butter. The nice warm syrup. And of course, you have to ask for some peanut butter to go on there too. (If you’re not putting peanut butter on your pancakes, you’re really missing out.)

Mama’s Pancake Breakfast (plus PB)

Today I want to talk about a less delicious, but more important stack (sorry pancake fans): the commercial real estate capital stack.

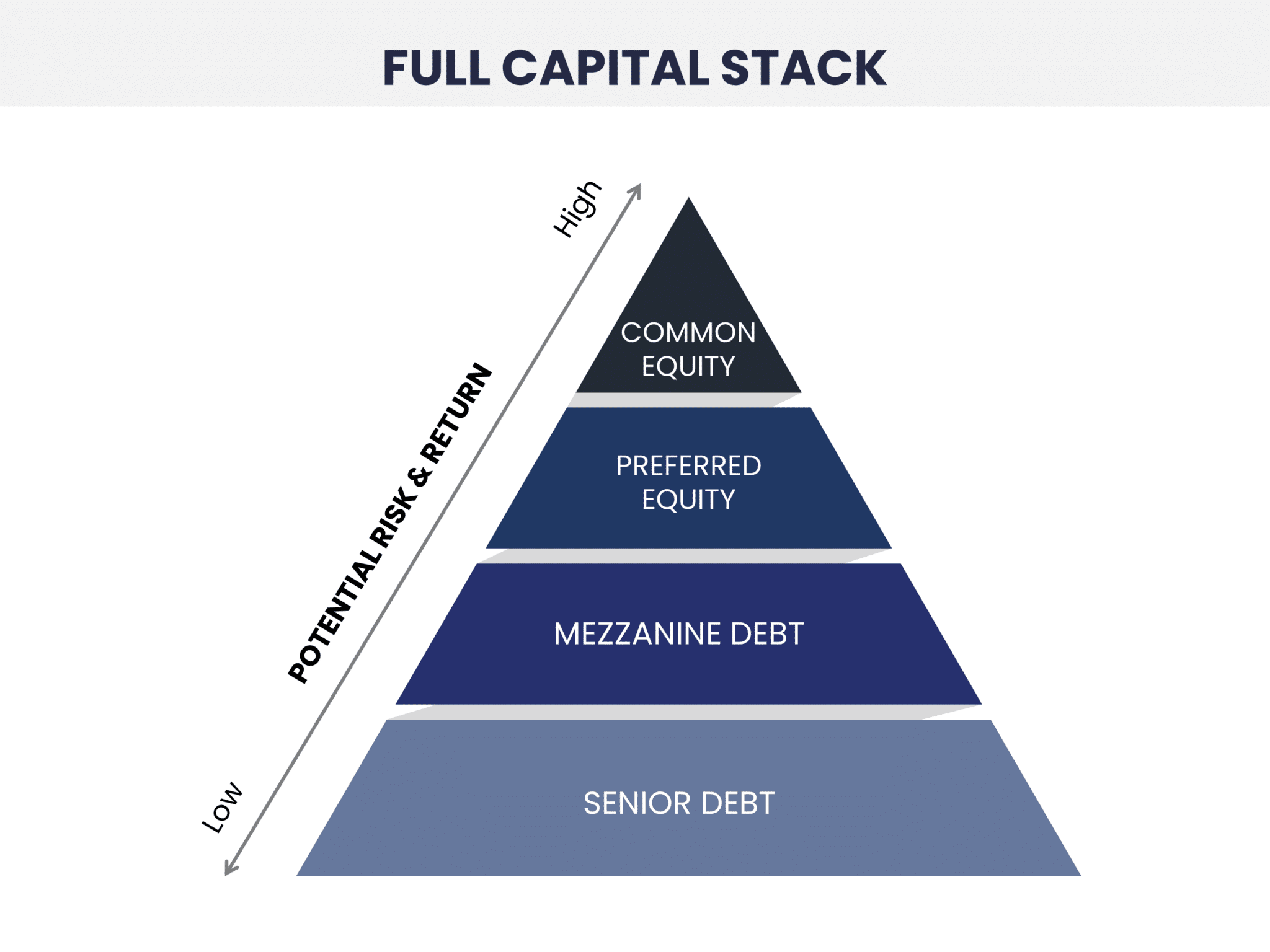

What is the capital stack?

The capital stack is the layered structure of financial contributions (capital) from various sources that fund real estate developments or acquisitions.

Each layer of the stack has its own rights, risks, and rewards. And as a passive investor, you should always understand the capital stack for any investment opportunity you’re considering.

Here’s a visual representation of a “full” capital stack showing the four common layers:

Image credit: CPI Capital

Let’s quickly go through each layer, starting at the bottom.

1. Senior Debt

In a typical commercial real estate deal, the senior debt (also called the first-position mortgage), comprises the majority of the stack, accounting for anywhere between 50-80% of the total capital. This debt is considered “senior” because it is secured by the property itself and has top priority in receiving any cash flow from the deal. The senior debt gets paid first and any remaining cash flow continues up the stack.

This makes it the lowest-risk layer. But that comes with a tradeoff: the potential returns for investors in this part of the stack (usually banks and other similar lending institutions) are capped. Once the senior debt is paid what is contractually owed (the monthly mortgage payment), it receives no further upside of the deal.

2. Mezzanine Debt

Just above senior debt is mezzanine debt, or mezz debt if you want to sound cool. Mezz debt can be secured by the property itself (a second mortgage) or by ownership interests in the property-owning entity. Since it is second in line to receive cash flows, it has increased risk and typically carries a higher interest rate than the senior debt.

3. Preferred Equity

The term “preferred equity” has become a vague catch-all for a hybrid of debt and equity. The structure and terms of preferred equity can vary wildly from deal to deal, but almost always include a fixed rate of return (think dividend) that must be paid before any remaining cash flow can continue up the stack.

Preferred equity holders have more upside exposure than the debt layers, but the returns are usually still capped at some maximum amount.

Important note: don’t confuse preferred equity with a preferred return on common equity. While there are similarities, the two are not the same.

4. Common Equity

At the top of the capital stack is common equity, which carries the highest risk but also the potential for the highest returns. Common equity investors are the last to be paid in any scenario, making the investment the most vulnerable to market fluctuations and project-specific risks.

However, the upside is significant and technically unlimited; once all other obligations have been met (the lower layers of the stack) common equity investors enjoy all remaining cash flows.

For individual investors evaluating an syndication investment opportunity, the portion of the capital stack being offered for investment is usually common equity. Unless the offering documents specifically say otherwise, assume your investment is in the common equity layer.

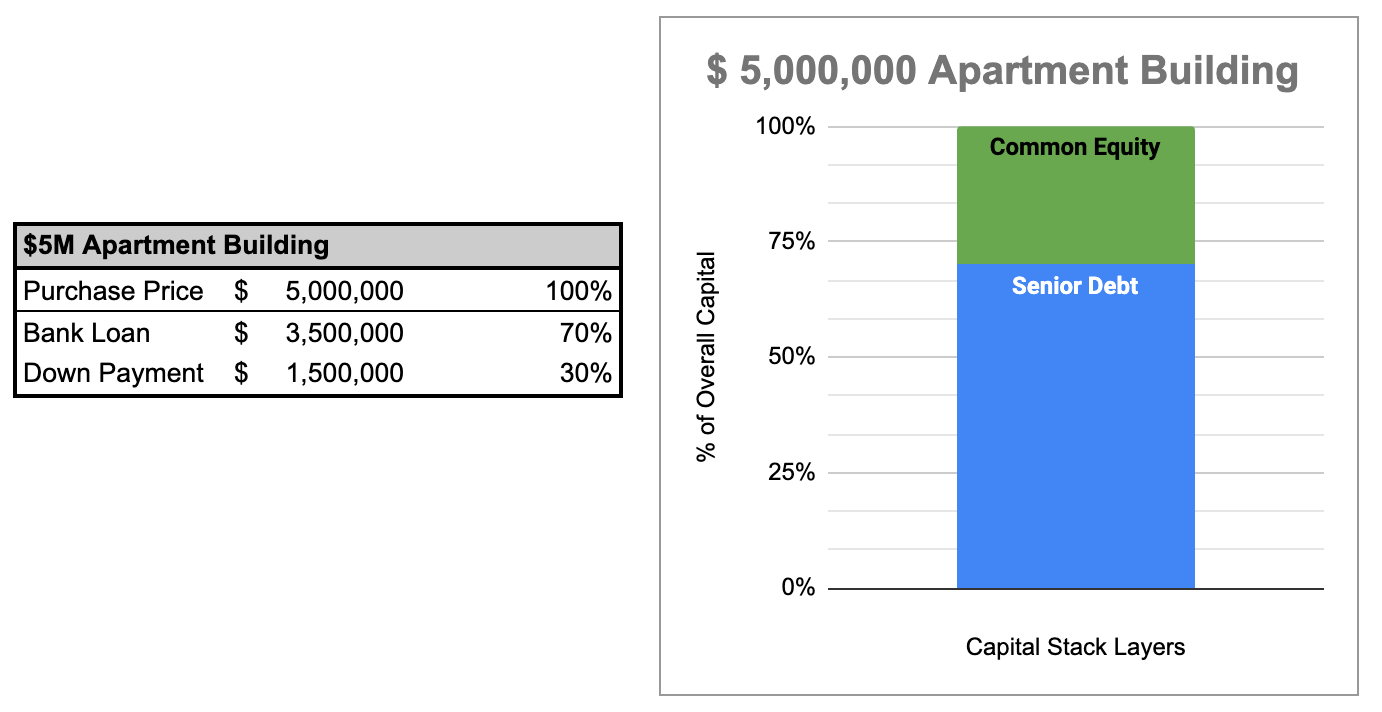

A simple example

Individual investors are less likely to encounter deals with mezz debt and/or preferred equity in the stack. More often than not, the capital stack in a real estate syndication includes just senior debt (the bank’s investment) and common equity (your investment).

Here’s a simple example: a $5M apartment building, where the syndication sponsor gets a loan from a bank at 70% LTV, and raises (syndicates) the common equity from individual investors:

The bank loan (senior debt) makes up 70% of the capital in the deal, and has first priority over any cash flows produced. But once the required debt payment is made, all remaining cash flows go to the individual investors (the common equity holders).

And the real beauty of real estate is that, thanks to inflation, a property’s income tends to increase over time. And since the debt payments are often a fixed amount, an increasingly larger share of the cash flows go to the common equity holders over time.

Understand the stack

As a passive investor, it’s critical to understand a deal’s capital stack and where your investment falls within it. As mentioned above, that’s most often common equity, so you’ll want to get a clear understanding of the layers sitting in front of you. Who else gets paid before you do?

The capital stack should be described in a deal’s offering documents, but if it’s not, be sure to ask the deal sponsor for clarification before investing.

Found this valuable? Join hundreds of sophisticated investors and receive these insights direct to your inbox every week.