PP024

Understanding IRR in Real Estate Syndication Investing

This week, I saw an older tweet from prominent multifamily syndicator Moses Kagan:

It struck a chord because it’s very relevant to some recent conversations I’ve had with investors about investment returns, specifically returns as measured by a commonly-used metric:

IRR.

What is IRR?

The Internal Rate of Return (IRR) is a measure of how profitable an investment is over time.

That last piece – over time – is important. It’s what sets IRR apart from other common investment return metrics.

IRR not only factors in the amount of return you received, but also when you received it. The longer it takes to receive a return, the lower the IRR.

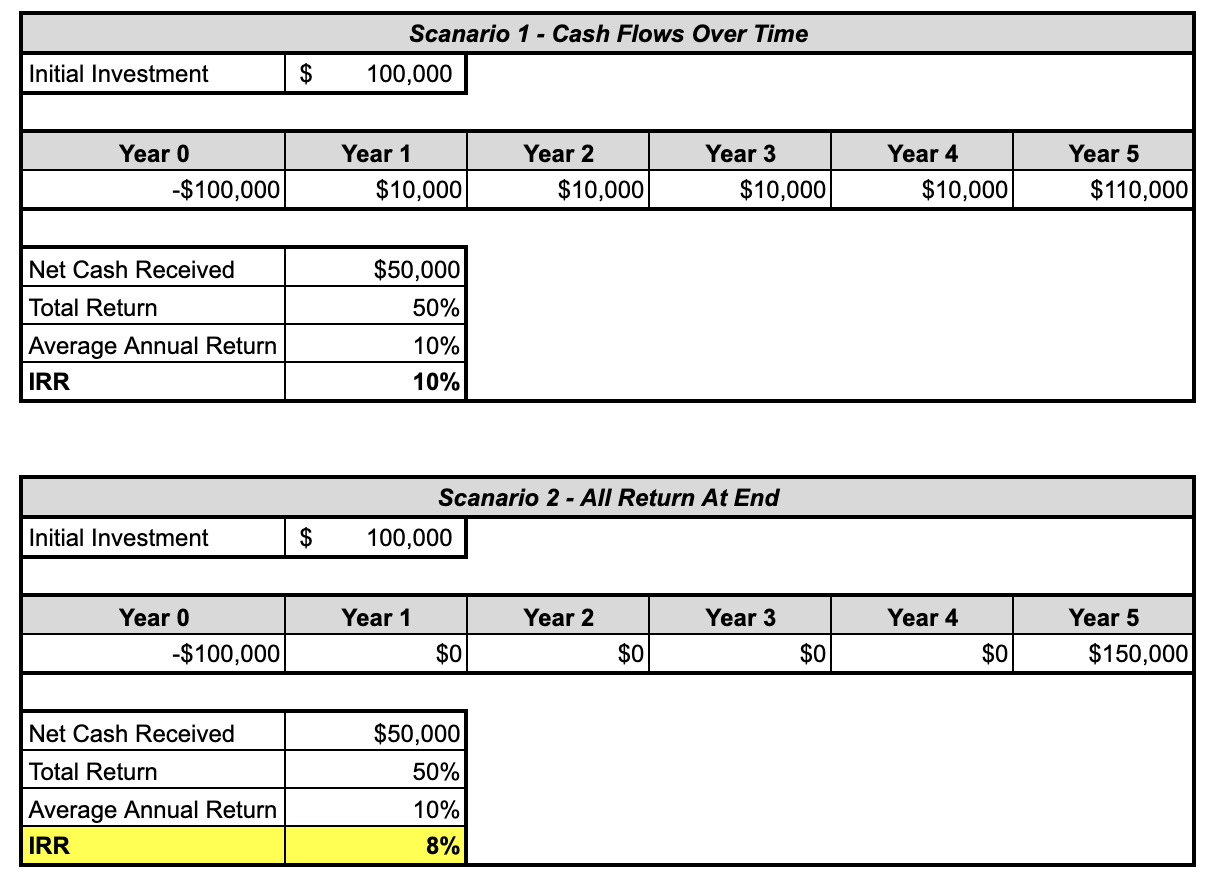

Here’s a quick example:

- The investment amount ($100K) and the total return ($50K) are the same in both.

- The total return ($50K / $100K = 50%) and the average annual return (50% / 5 years = 10%) are the same in both.

- The IRR is lower in Scenario 2 because all of the cash flows (returns) occur at the very end.

Why investors like IRR

The IRR metric is popular for one reason: it’s flexible.

Since it only looks at cash flows and their timing, it can be used to compare returns on a wide variety of investments, anything from real estate to stocks to business expansions.

But this ability to apply IRR to myriad investments (and theoretically “compare” them with each other) is actually the source of its issues.

The problems with IRR in real estate syndications

When applying IRR to real estate syndications, several pain points arise:

1. IRR mashes all investment returns together

IRR doesn’t differentiate between cash flow distributions and property appreciation.

If most of a deal’s returns come from appreciation (realized through a sale or refinance of the property after 5+ years), but what you really wanted was consistent cash flow through the life of the deal, you have a potential problem.

A deal with a “good” IRR might actually be a bad match for you, based on your personal preferences and goals.

2. IRR doesn’t accurately account for risk

Because IRR is a mashup of all returns from a deal, it can easily obfuscate the true level of risk present.

You need to understand the assumptions driving the returns. Annual rent growth is an important assumption for cash flow, and cap rates / interest rates are critical for appreciation. Which leads into the biggest issue…

3. Real estate IRRs require an accurate forecast of interest rates

Commercial real estate (like an apartment building) is valued using two components:

- Net operating income (NOI): rents minus expenses. Note that debt service / mortgage payments don’t factor into NOI.

- Market cap rate (short for capitalization rate): a property’s cap rate is its NOI divided by its purchase price. The market cap rate represents the average cap rate of recent comparable sales within that market (a geographical area).

While actual market cap rates are determined by looking at recent transactions, they’re heavily influenced by interest rates in the broader financial markets, and tend to track the yields of the US 10-Year Treasury bond.

In order for a syndication sponsor to forecast what their property will sell for in 5+ years, they have to forecast both NOI and market cap rate. NOI is largely within their control, but no one can control market cap rates.

So if a significant portion of the IRR is driven through realized property appreciation, the IRR is essentially a gamble on how accurately the sponsor can predict future interest rates.

Very few people can do this well. And those who actually can are usually trading bonds for big Wall Street banks, not syndicating apartment buildings.

IRR is a metric, not the metric

A few takeaways here:

- Don’t “shop” investments based solely on IRR.

- Make sure that a deal’s return structure aligns with your goals. Know how much of the IRR comes from cash flow vs. appreciation. The IRR number itself won’t tell you this.

- Always ask sponsors about the assumptions in their returns, especially the exit cap rate or refinance interest rate.

- Remember that if most of a deal’s IRR is driven by a sale or refinance, the IRR represents the sponsor’s guess about an uncontrollable factor in the future.

Found this valuable? Join hundreds of sophisticated investors and receive these insights direct to your inbox every week.