PP054

REITs Are Not Real Estate

Here’s something I often hear from investors who've only ever invested in the stock market:

“If I want passive exposure to real estate, why not just buy a REIT instead of investing in a syndication? I can buy REITs in my IRA/brokerage account and they give me liquidity."

It's a reasonable question.

But there's a fundamental flaw in this thinking:

Public REITs are not real estate. They function much more like stocks – and this distinction matters more than most people realize.

The Hidden Cost of Wall Street

Here's something that might surprise you:

Only about 85 cents of every dollar invested in a public REIT actually ends up in property. The other 15% disappears into the "Wall Street machine."

This happens because REITs have two distinct layers of expenses:

- Standard property costs (acquisition, management, maintenance, etc.)

- Corporate overhead (executive salaries, SEC compliance burden, listing fees, etc.)

Now, I'm not suggesting syndications don't have fees – they absolutely do. But they're typically transparent and tied directly to performance. In a normal single-asset syndication, 95%+ of your investment goes straight into the real estate and direct acquisition costs.

When Your "Real Estate" Acts Like a Stock

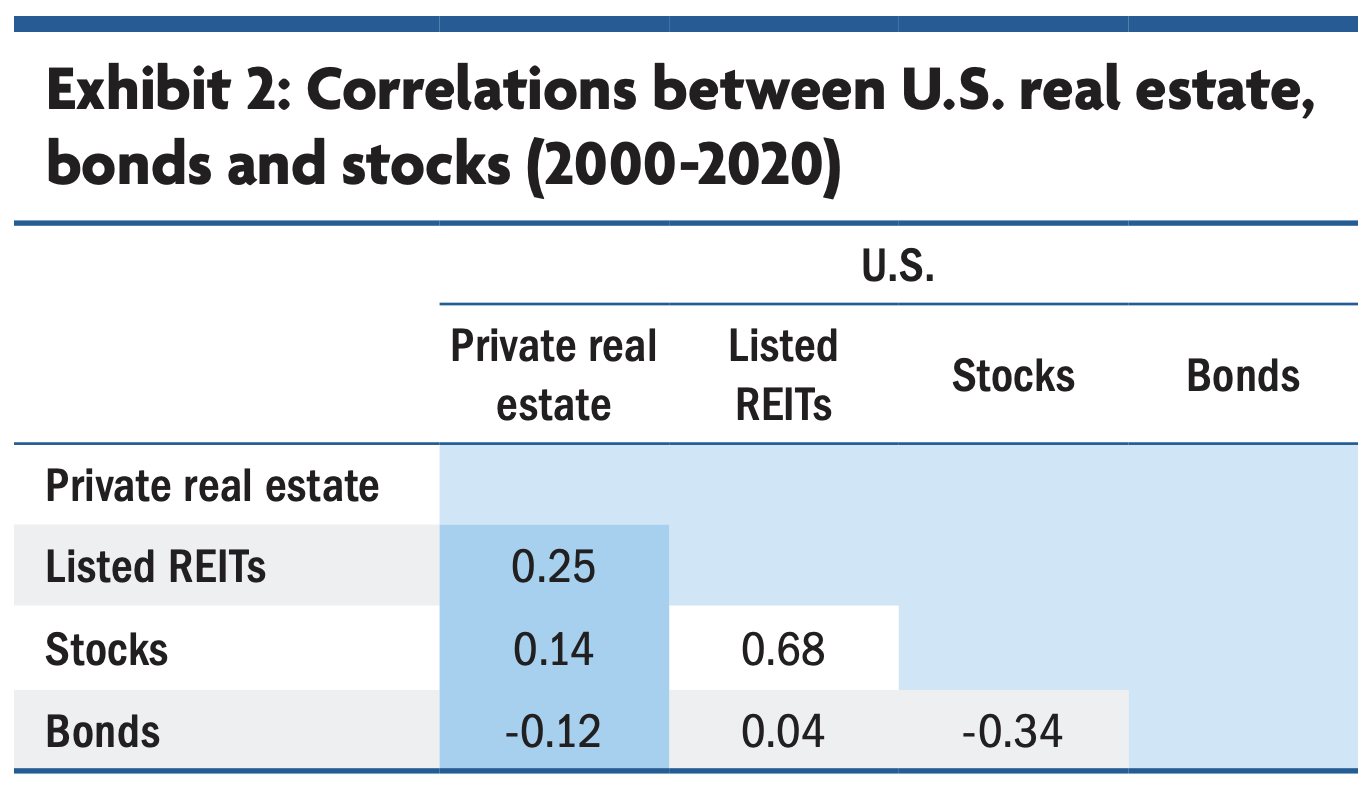

Research from insurance and investment company TIAA revealed something fascinating:

Over a 20-year period, public REITs showed a 0.68 correlation with the stock market.

For the non-finance folks, that means if the S&P 500 drops 10%, your REIT is likely to drop about 6.8%.

Private real estate? It has just a 0.14 correlation with stocks. Translating again, that means there’s basically no correlation between stocks and actual real estate.

In other words, private real estate tends to move independently of what's happening in the stock market.

Source: TIAA

So what does all this mean in practical terms?

When the stock market has one of its periodic meltdowns, your "real estate" investment in REITs is going down with it – even if nothing has changed about the underlying properties.

The Dark Side of Liquidity

"But at least I can sell my REITs whenever I want!"

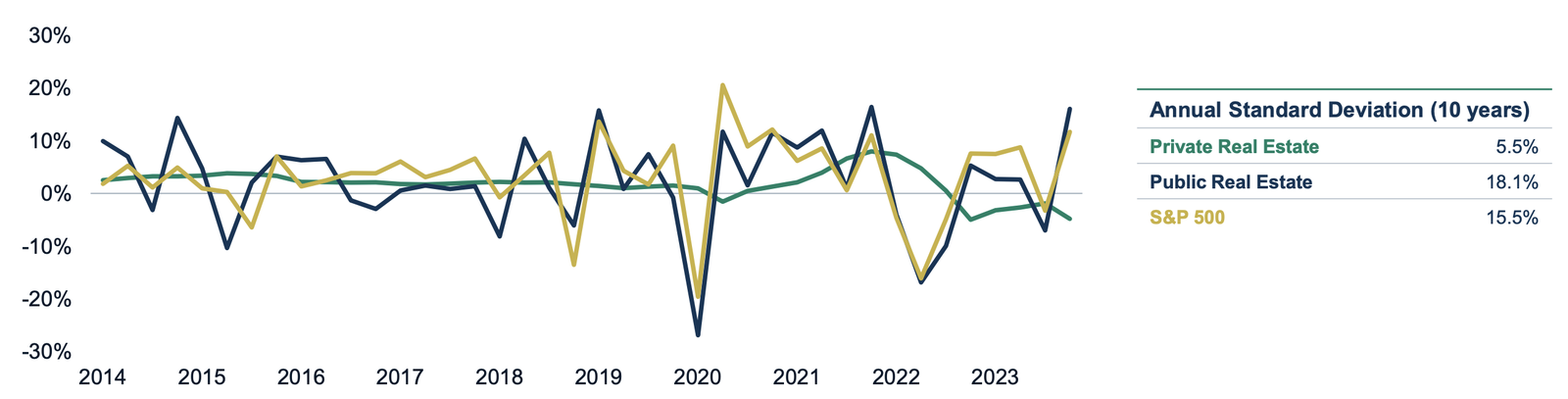

True. But that liquidity comes at a price: volatility that's much higher than what you see in private real estate.

Over the past two decades, the annualized volatility of the S&P 500 has typically hovered around 15–20%, while private real estate (as measured by the NCREIF Property Index) has volatility closer to 5–8%.

Source: Brookfield Oaktree

This hits home for me personally. I'm the type of investor who struggles not to check account balances daily. And when I see big drops, my lizard brain starts screaming "SELL!"

That's one big reason I've grown to appreciate the illiquidity of syndications. It protects me from my worst instincts.

When you can't panic-sell during a downturn, you're forced to stick to your long-term strategy.

Why Illiquidity Can Be Your Friend

Here's where private real estate's "disadvantage" becomes a strength:

Its illiquidity actually protects you from making those emotion-driven decisions.

Without constant mark-to-market pricing driven by Wall Street trader sentiment and market fear, you're less likely to make snap decisions that hurt your long-term returns.

The Bottom Line

So if you find yourself saying "I want a passive real estate investment" and you go buy REITs, understand what you're really doing: buying a stock that happens to own real estate.

For truly passive real estate investing, syndications offer:

- Lower fees

- Better risk-adjusted returns

- Insulation from stock market volatility

- Protection from emotional trading decisions

Yes, syndications have higher minimum investments and less liquidity. But if you're looking for genuine real estate exposure and more stable long-term returns, these "downsides" might be exactly what your portfolio needs.

Found this valuable? Join hundreds of sophisticated investors and receive these insights direct to your inbox every week.