PP011

The Truth About Real Estate Distress in 2024

Match 22, 2024

For the better part of the last two years, there’s been much talk about the coming opportunities to buy distressed real estate on the cheap.

The general thesis: a return to pre-pandemic norms combined with the Fed’s unprecedented interest rate hikes would create Great Recession-level distress in real estate. It would be a “buy when there’s blood in the streets” opportunity, as Buffet says.

I vividly remember attending a conference in March 2022 where one of the speakers clearly and methodically laid out the case for the incredible deals that would come in “18-24 months.”

Well…it’s been 24 months since that presentation, and myself and lots of others are still looking for those deals to show themselves.

Now to be fair, there’s absolutely been distress in real estate, especially over the last year. And some folks are picking up great deals here and there. But the distress we’ve seen so far is nowhere near the scale that was predicted.

So what happened?

I was full-on in the camp of “prepare for the generational buying opportunity” so I’ve been reflecting on this recently.

And as if hearing my thoughts, Marcus & Millichap recently published a couple of research pieces touching on this topic.

Background

By now, I’m sure you’ve heard the phrase wall of maturities.

If not, here are the highlights:

- There was/is a massive amount of commercial real estate debt maturing in 2023-2025

- This debt was originated at significantly lower rates than now

- Borrowers won’t be able to refinance at higher rates

- Pandemonium ensues, opportunities abound

It makes logical sense. But of course, like any extrapolation, it doesn’t account for unforeseen events. Or in this case, government guidance.

Several government agencies issued guidance to lenders last year basically saying “go easy.” In other words, work with borrowers, don’t just write off the loan and/or foreclose. Plus, it’s in a lender’s best business interest to do so.

By early this year, it started to look like the wall of maturities was more likely to be a speed bump.

Where did the debt go?

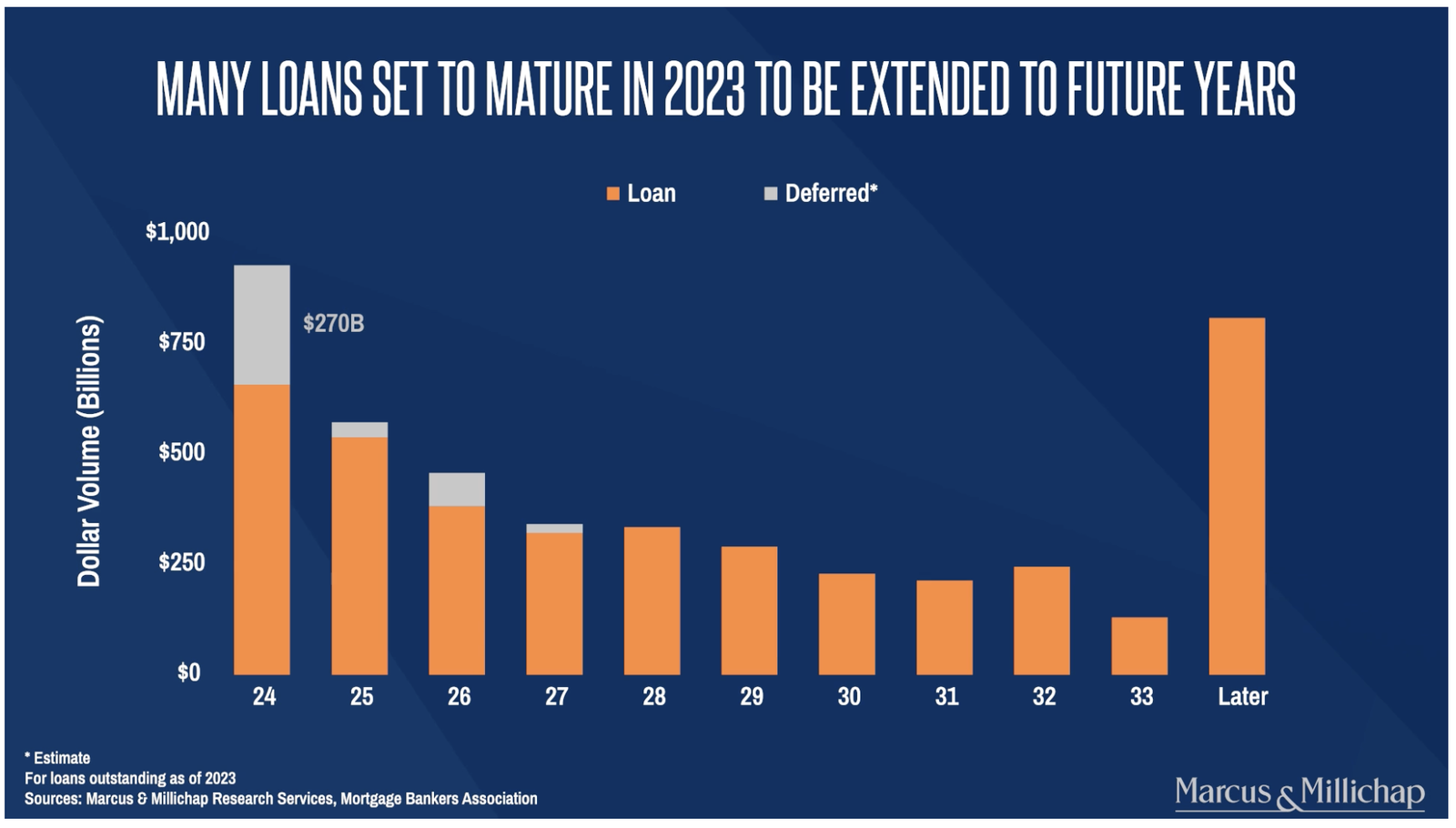

Marcus & Millichap put together a chart showing how much of 2023’s maturities they think was pushed into future years (by comparing older data and estimating how much of the growth in maturities was due to deferrals vs. new originations).

They estimate a whopping $270B of CMBS loan maturities were deferred to 2024 alone.

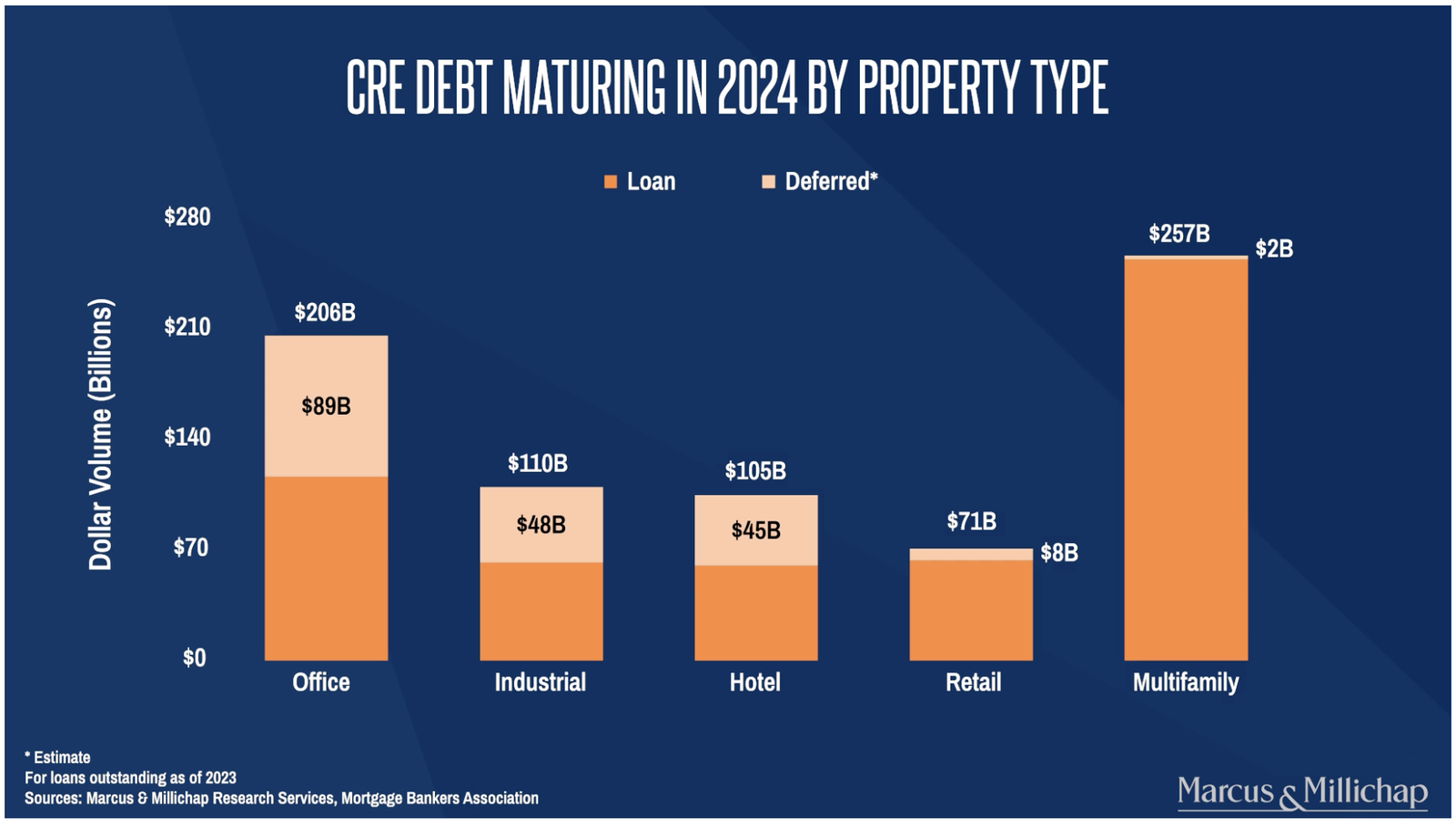

But what’s more interesting is the breakout of that debt by property type:

Nearly a third was debt on office properties, further confirming that a significant amount of current distress is confined there.

Also interesting is that only 1% of the deferrals was for multifamily/apartments.

Speaking of apartments…

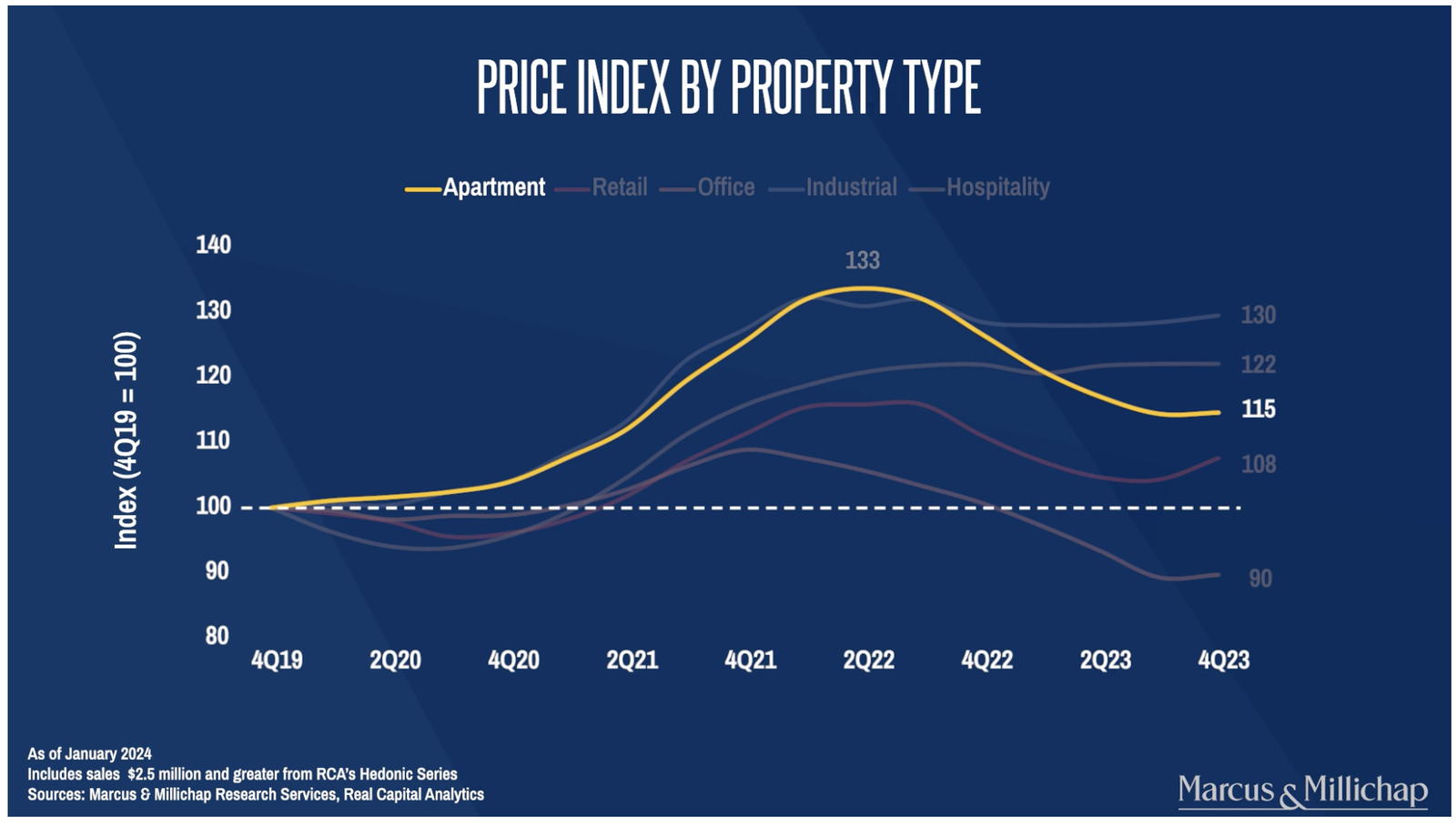

In a separate research piece, Marcus & Millichap created a price index graph, showing changes in prices by property type, indexed to values in Q4 of 2019.

A few takeaways from this:

- Overall apartment values are down ~15% from the peak in 2022, but are still up 15% from pre-pandemic levels. Accordingly, only the loans on properties purchased at the peak are the most likely to be in trouble.

- Apartment values have stabilized over the last 9 months, even ticking slightly higher.

- Office values have stabilized as well but are still below 2019 values, significantly contributing to the loan distress there.

Final thoughts

With each passing month, we get a clearer sense for how severe this “down cycle” will be. And more and more evidence is indicating that distress will be relatively limited overall, concentrated in only a few areas.

It looks like most of the folks, myself included, who were waiting to pounce on distressed properties left and right are better suited to reset and instead focus on emerging upside opportunities.

Of course, an argument can be made that it’s still too early, and the real distress is just around the corner.

And that may be true. But at some point, the folks saying that are no longer early - they’re just wrong.

Found this valuable? Join hundreds of sophisticated investors and receive these insights direct to your inbox every week.