PP097

2026 Multifamily Outlook

I spent way too much time this week looking at charts.

Not because I love staring at bar graphs and trend lines (though I kinda do), but because Marcus & Millichap dropped their 2026 multifamily outlook. And the picture they paint?

It’s...complicated.

If I had to summarize it in one sentence: short-term choppy, long-term favorable.

It’s not exactly a clean, simple forecast. But it appears to be accurate for the environment we’re in. And since you’re reading this newsletter, I’m guessing you’d rather have an honest assessment than a sugar-coated prediction.

So let’s talk about what’s actually happening in multifamily right now.

The Headwinds

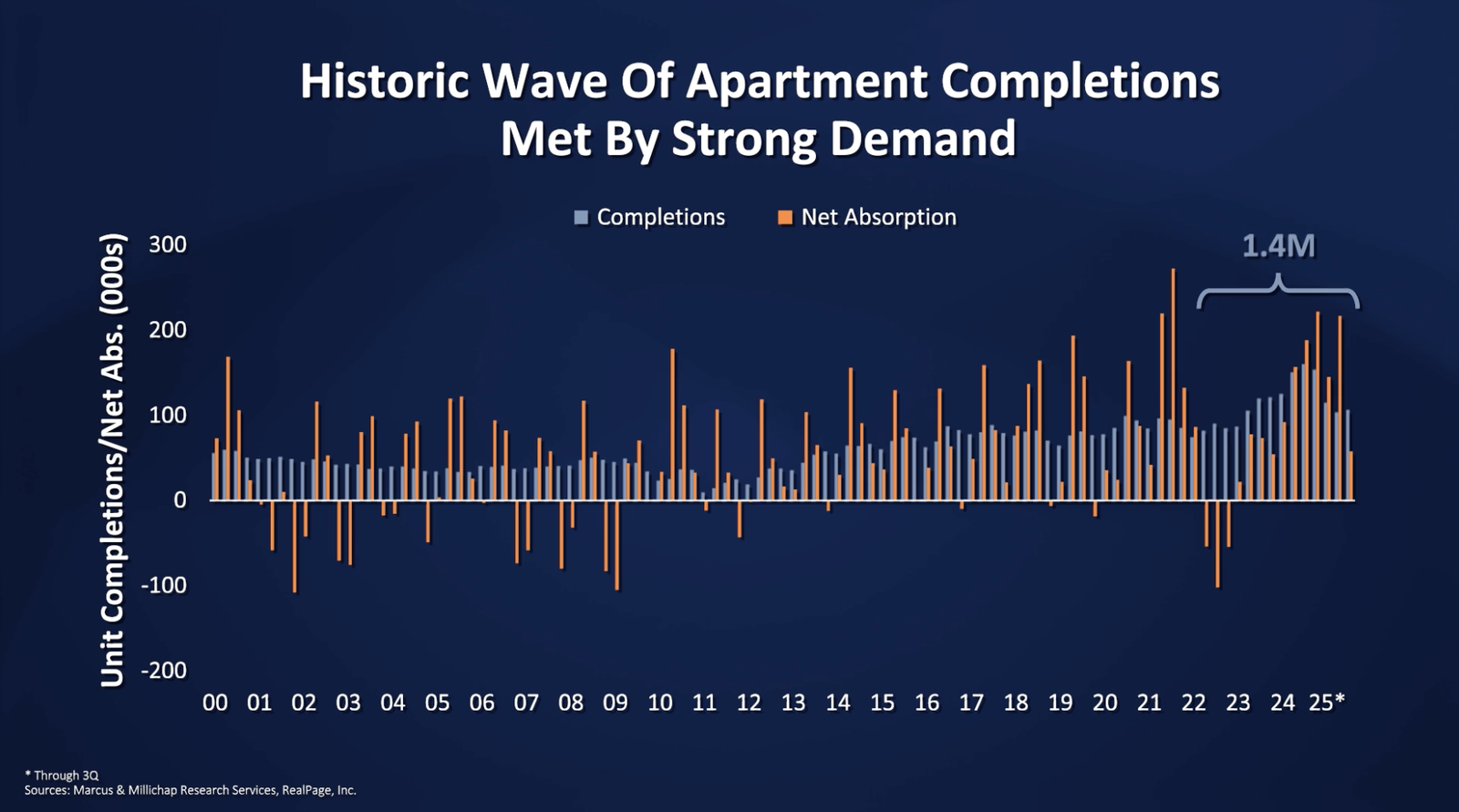

One of the biggest stories here is the absolute boatload of new construction that happened over the last three to four years.

We saw an incredible amount of new apartment deliveries. And for a while, record absorption met that record supply – demand was insane, so vacancy stayed lower than anyone expected.

But demand has weakened nationally.

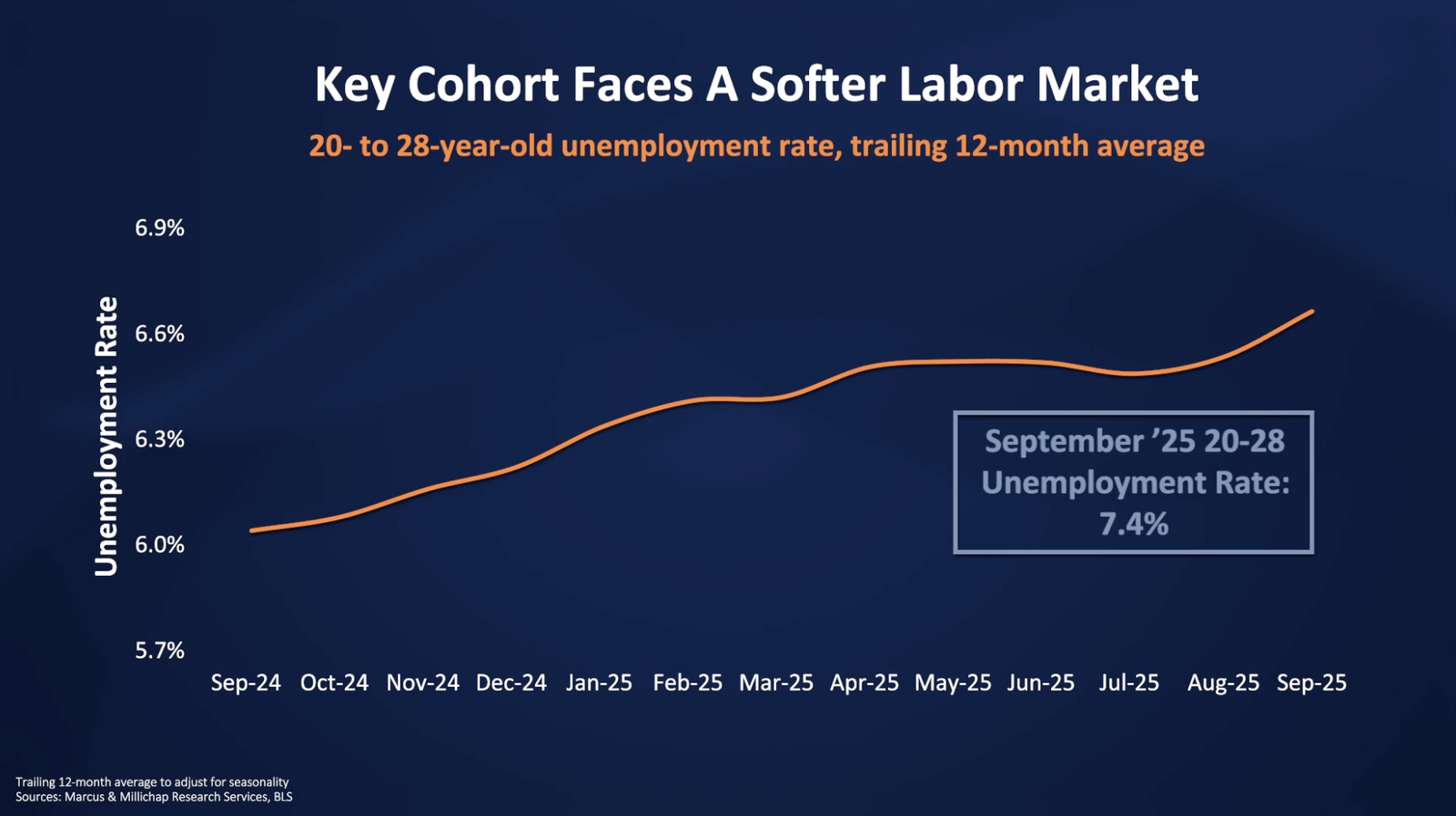

A big driver is unemployment in the 20-28 age cohort – prime renting age. It's pushing 7.5%, well above the national average. Couple that with consumer sentiment that's been in the gutter (the University of Michigan index has been falling most of the year), and you get a nasty combo: fewer people forming households.

Reduced household formation = reduced demand for housing, including rentals.

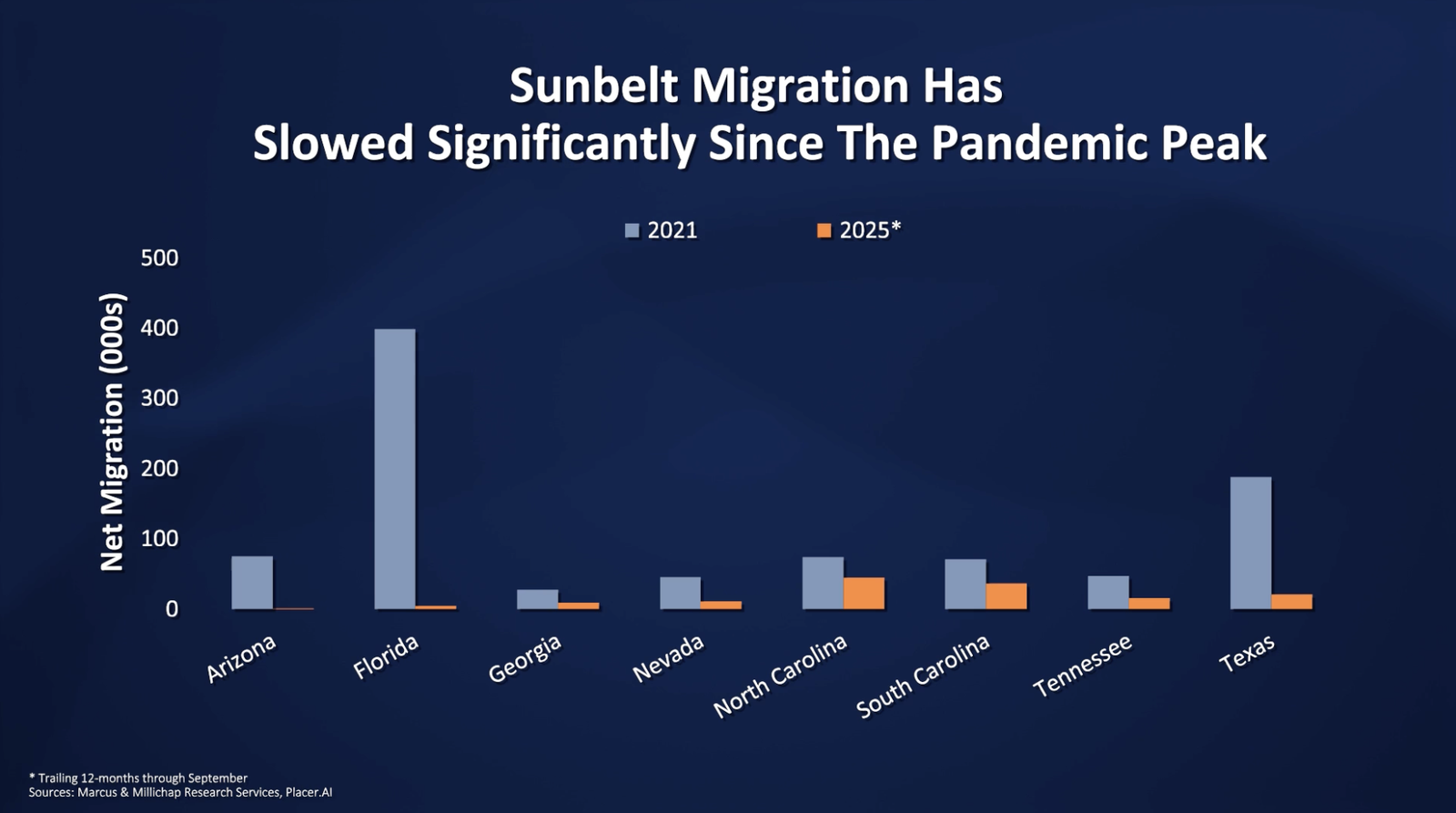

The markets feeling this the most are the Sunbelt darlings everyone piled into post-pandemic. Austin and Nashville are poster children, but Charlotte and Phoenix are right there too. These markets had massive new construction pipelines and benefited from huge migration waves in 2021-2022.

But that migration has slowed significantly. Marcus & Millichap's charts comparing 2021 to 2025 tell the story: the stampede to the Sunbelt is over.

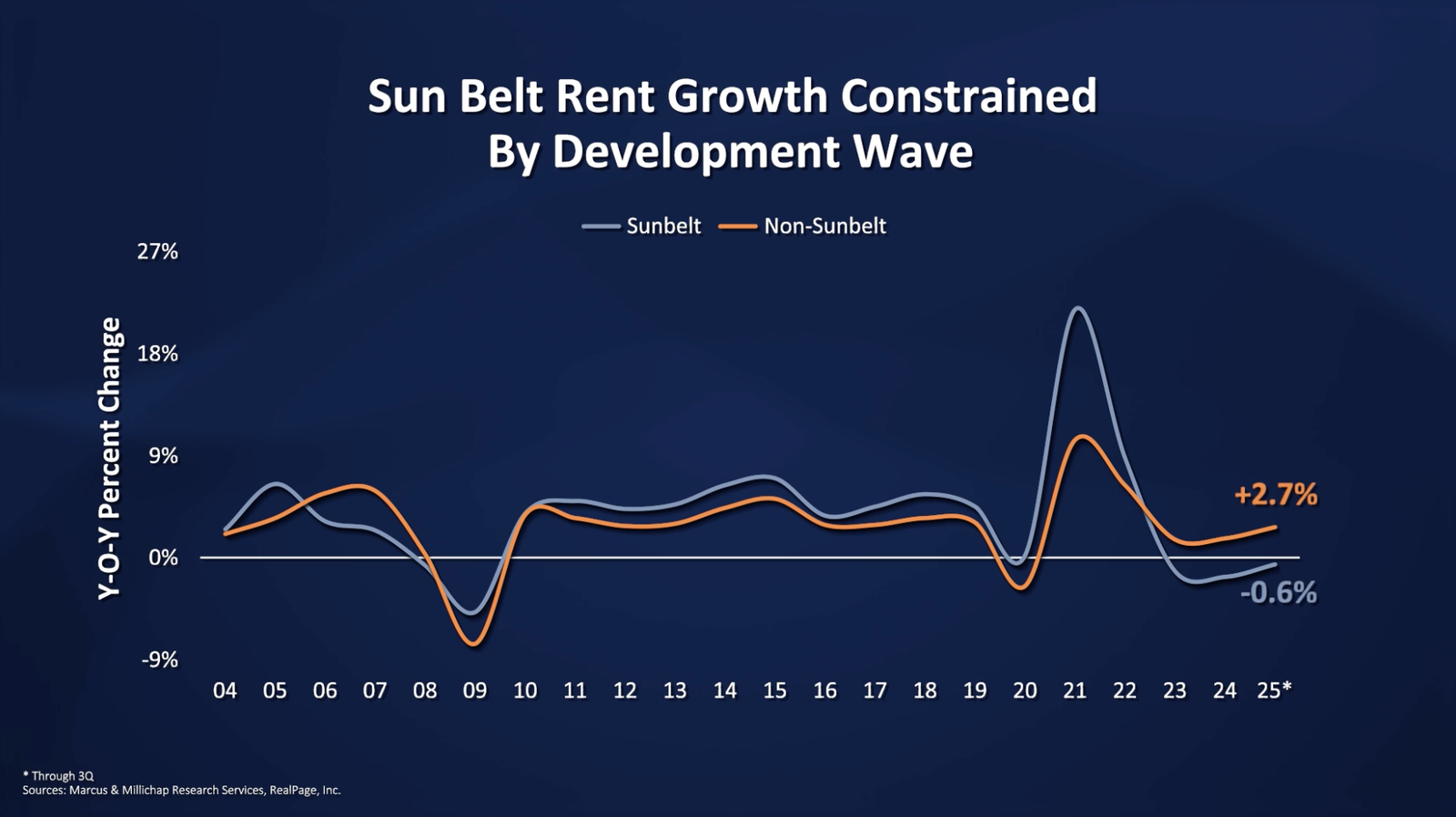

Result? Many of these markets are dealing with lots of concessions and flat or negative rent growth, while the rest of the country is seeing modest, but still positive, growth.

Not fun if you’ve invested in one of those markets betting on continued aggressive rent bumps.

The Tailwinds

Now for the good (or at least better) news.

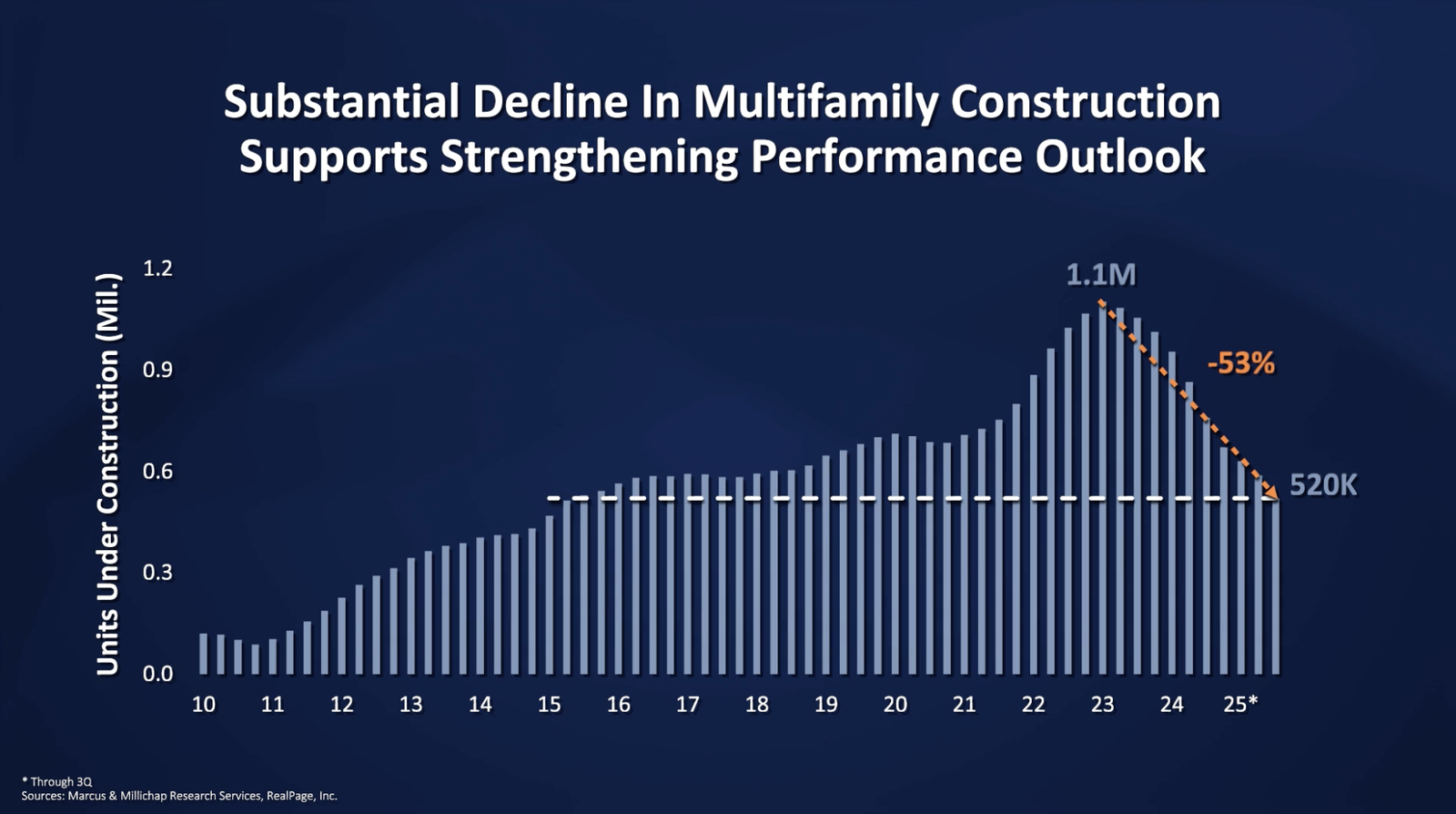

First, new construction is down over 50% from its peak, back to 2015 delivery levels. That’s a significant drop that helps on the supply side.

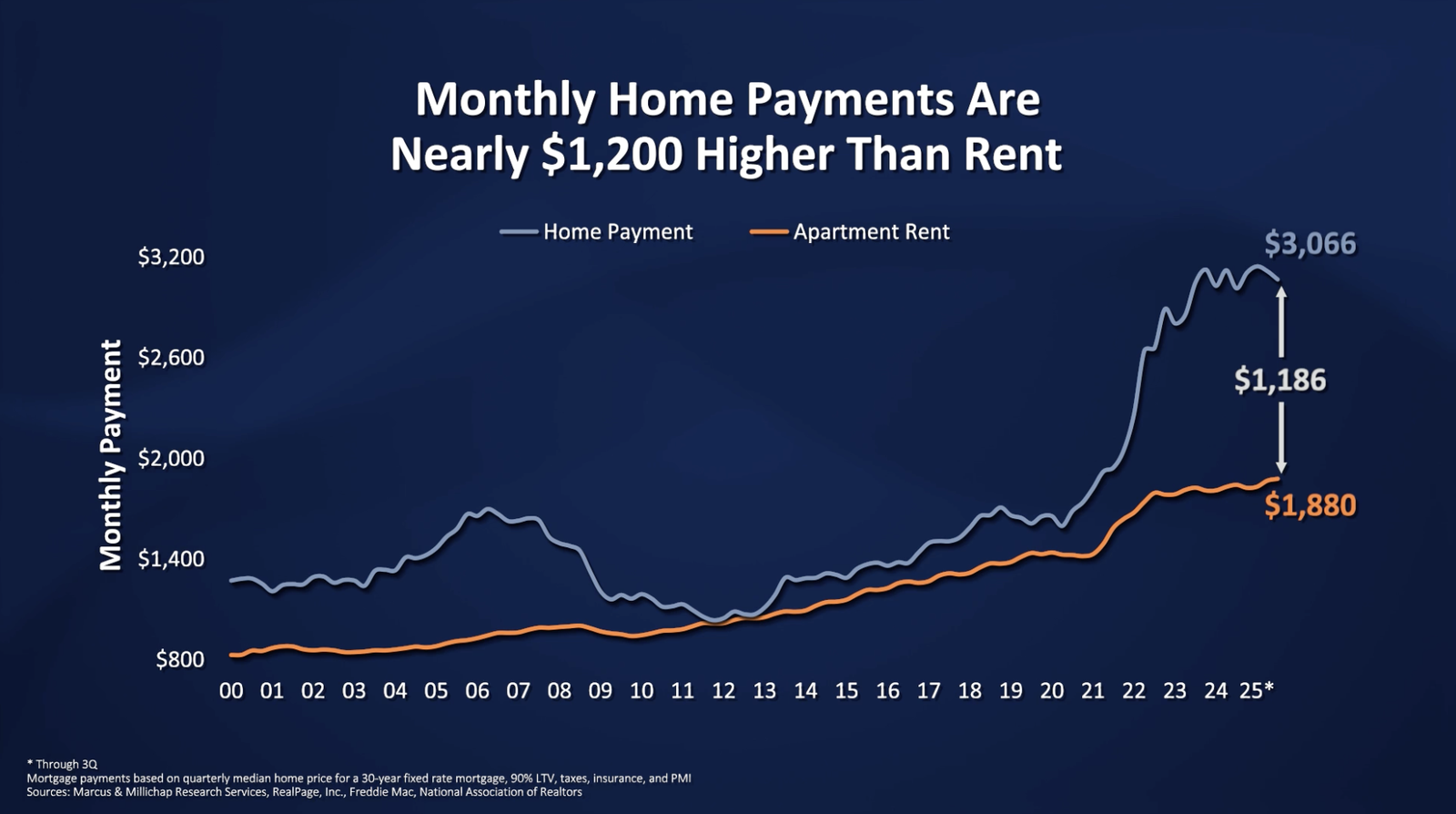

Second, home affordability remains terrible. The average rent payment is about $1,200 less per month than the average new mortgage. That gap is keeping people in rentals longer.

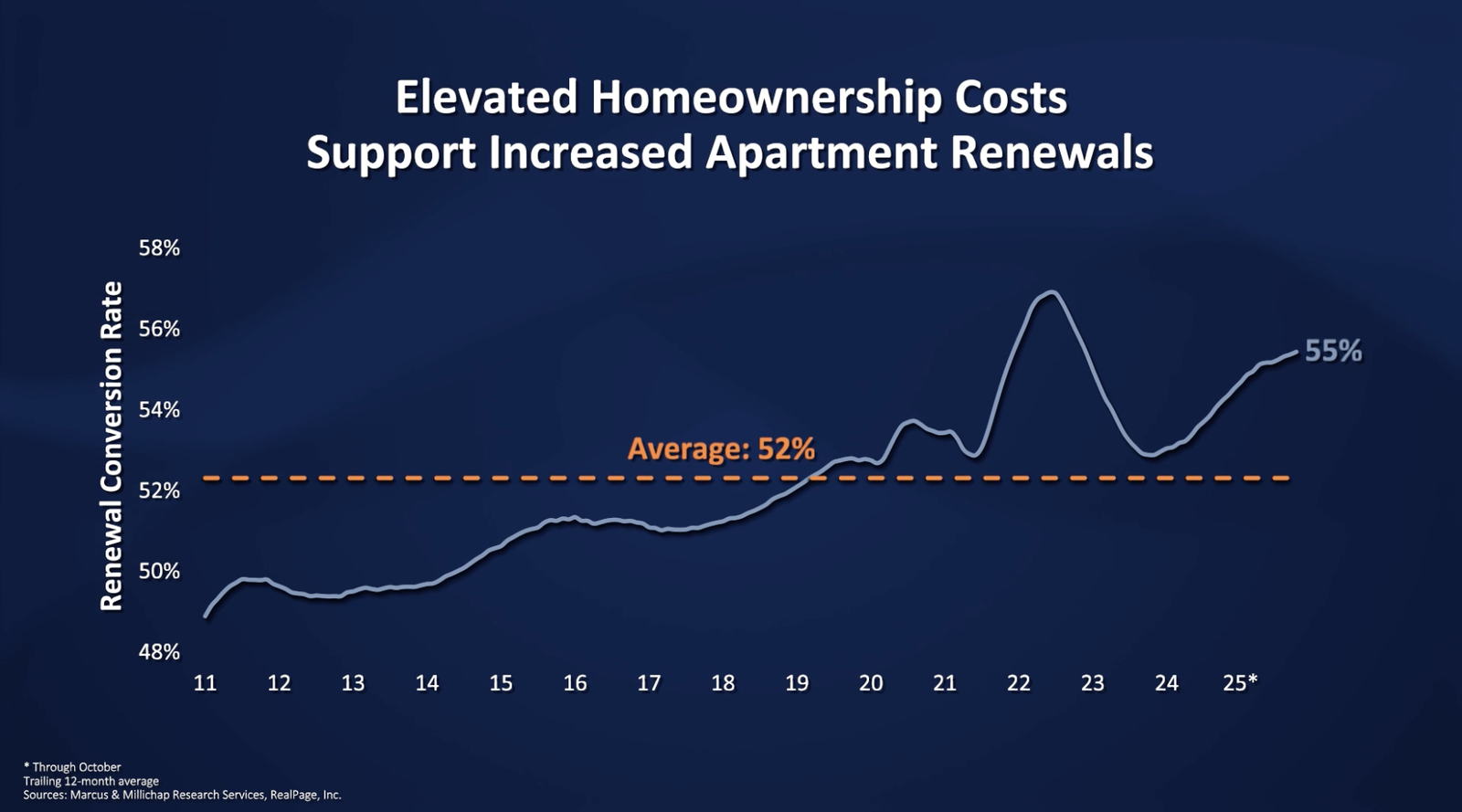

You can see this in apartment renewal rates. They’d been dropping post-pandemic but bottomed out and are now ticking back up.

Third, there’s also reason to think household formation could improve. Consumer sentiment actually rose in December for the first time since the summer, and we got an unexpectedly positive jobs report (JOLTS) earlier this week.

If uncertainty decreases (a complex if), household formation should pick back up. Which boosts demand. Which boosts rents.

Fourth, new construction isn’t coming back in force anytime soon. Interest rates, materials costs, and labor expenses make new developments nearly impossible to pencil.

Which constrains supply. Which boosts rents.

What This Means for You

No one has a crystal ball, least of all me. But I just don’t see a multifamily crash coming. The supply and demand dynamics don’t support it.

So the big questions are around timing.

- How long will those overbuilt Sunbelt markets take to recover?

- When does consumer sentiment meaningfully improve?

- What happens with jobs and hiring?

All unknowns.

But here’s what’s very clear from this data…and what you should care about if you’re evaluating deals as a passive investor right now:

Be extremely cautious about any multifamily deal in a market that had heavy construction over the last few years.

These markets will recover the slowest. Rent growth will be subdued for several years. If a sponsor is projecting 2-3% annual rent growth starting in year two or three? Push back hard. Ask them to defend those assumptions.

That doesn’t mean there aren’t good deals in these markets. But the returns will likely come from near-term value-add opportunities or acquisition at an attractive basis – not from betting on massive rent growth.

Where I Land on This

I think the tailwinds outweigh the near-term headwinds. The fundamentals for multifamily remain strong – we have a housing shortage, new construction is constrained, and people can’t afford to buy homes. This creates a favorable long-term environment.

But it definitely isn’t 2021 anymore. Market selection and underwriting assumptions matter more than ever.

If you’re looking at deals, don’t be afraid to ask the hard questions, and pass if the numbers feel aggressive. There will always be another deal.

But it’s hard to recover from putting capital into a mediocre sponsor chasing rent growth that isn’t coming.

Found this valuable? Join hundreds of sophisticated investors and receive these insights direct to your inbox every week.